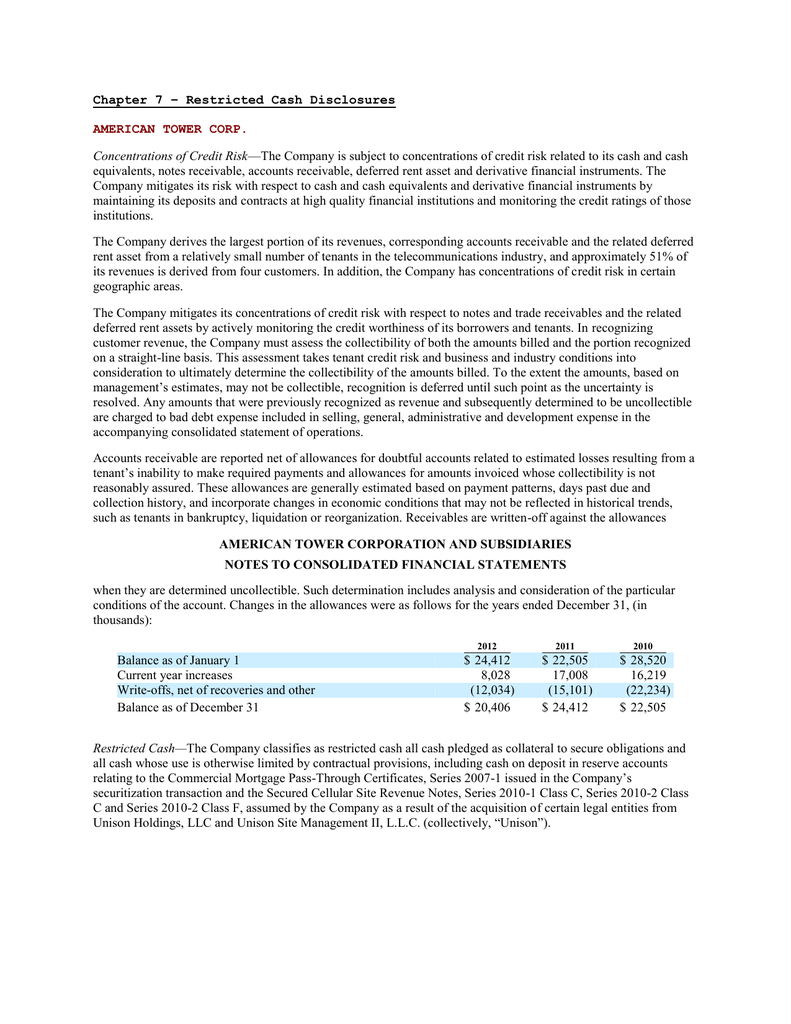

Your residence is the premier purchase you actually ever generate. Choosing to purchase a property is a significant decision, therefore it is important to ensure it is a considerate solutions installment loans online in Kentucky too. Finding the time to understand just how qualifying for an interest rate works will help improve process once the fulfilling because fun.

After you get your loan, mortgage brokers will look from the various recommendations. It sooner comes down to these around three something: your own borrowing from the bank, income, and you can assets.

step 1. Your Credit

Loan providers tend to opinion your history which have a consult with the around three big credit agencies TransUnion, Experian, and Equifax. Everything they gather can assist them take advantage advised decision from the financial degree processes.

Near to your credit score is a computed credit score, also known as a great FICO score. Your credit score vary between 3 hundred-850.

Lenders lay their particular criteria for just what score they’ll deal with, but they essentially consider carefully your pay record, if the costs were made punctually, and when the loan was paid off completely.

Your credit score is a determining factor with home financing qualification, plus it facilitate determine the pace that you will get. The higher your get, the simpler its so you’re able to be eligible for a mortgage.

Now that you’ve got an insight into borrowing, you may inquire how exactly to replace your rating. Envision each other your credit rating and report the amount appear from as well.

Find problems or loans wide variety noted that do not end up in you. If you get a hold of problems, take time to get in touch with the brand new creditor and disagreement all of them truthfully. New creditor’s info is on the report having simple reference.

2. Your income

2nd, your earnings in addition to things throughout the qualification process. Lenders usually determine your debt-to-income (labeled as DTI) proportion. Your DTI comes with any fixed expenditures – expenses which might be an equivalent number per month – plus the the new home loan.

This type of expenses is following examined up against their disgusting month-to-month earnings (before any taxes was subtracted). This helps your own bank determine whether would certainly be saving money as compared to demanded 50% of your gross monthly income to the the individuals repaired expenditures.

Ranged costs particularly resources, cable, or mobile phones are not within the DTI proportion. You could potentially bookmark this as an instant reference having terminology to help you understand throughout the processes.

3. The Assets

Possessions also are important to the new qualification processes. Property was things you individual which have a monetary value. Thus, any cash you have during the account that could be taken away since cash shall be listed as the a valuable asset.

Bodily assets can be offered to possess funds to better qualify for a home loan. These assets are, however they are not restricted so you can, points instance properties, property, trucks, ships, RVs, accessories, and you will artwork.

The financial institution ple, they’ll must be sure the total amount you will be having fun with on the down payment is obtainable for the a h2o dollars account, for example a monitoring or savings account.

In addition to, with regards to the variety of funding you may be trying to, there can be a requirement to have a stable bucks set aside. Reserves range from possessions given that a hold is what you have remaining before generally making a deposit otherwise expenses one settlement costs. These set-aside conditions be much more preferred of trying to acquire a great 2nd domestic or investing a home.

Tying It To each other – See Your loan Models

We talked about the importance of the FICO rating before, but it is beneficial to remember that certain mortgage loan sizes enjoys independence in the scoring certification.

A traditional loan are home financing perhaps not funded of the a national company. Most conventional funds is actually supported by home loan enterprises Federal national mortgage association and you can Freddie Mac. The average minimum FICO rating regarding 620 is usually necessary whenever applying for a conventional loan, but loan providers always make their very own dedication about.

Virtual assistant fund is actually protected because of the You.S. Service away from Veterans Things. They have been intended for pros, active-responsibility army users, and qualified thriving partners. The fresh Virtual assistant doesn’t place the very least credit rating for those financing, and you can loan providers can form their particular standards.

Mortgage loans backed by the latest Government Property Government (FHA) are capable of first-go out homebuyers and you may reduced-to-reasonable earnings individuals. This type of loans need reduced off payments than other sort of mortgage loans.

The U.S. Department regarding Construction and you will Urban Development says you may want to qualify for an FHA mortgage that have a credit rating regarding five hundred provided that since you lay out about 10%. Having increased FICO credit score-no less than 580-you can even meet the requirements that have a down payment as little as step 3.5%.

Deeper Colorado Borrowing from the bank Commitment Mortgages

On Greater Texas Credit Relationship, all of us is preparing to help you prefer a mortgage loan to match your demands. We realize being qualified for a home loan was an alternate process. Plus it seems different for everybody given credit, assets, and earnings may vary.

Click less than for additional info on taking a mortgage loan away from a credit Union. Or write to us if you have questions. We have been constantly right here to aid!