- This new Freddie Mac CES financial unit doesn’t align on construction purpose of GSEs. An analysis of argument displayed lower than verifies it, in fact, will not appear to match their property goal.

This short article today dig more deeply towards the around three subjects conveyed more than for further dialogue and you can investigation: (1) assessing the amount of borrowing exposure so you can Freddie Mac computer; (2) comparing whether or not providing CES mortgage loans aligns into the goal of your GSEs; and (3) investigating how good the personal market already offers collateral extraction financing facts.

Freddie Mac’s proposition is through buying repaired-price CES mortgage loans which have a keen amortizing 20-season maturity. The terms are specifically made to line-up the financing threat of the new CES home loan for the exposure already consistently acknowledged from the Freddie Mac in the event it do an earnings-away refi. Thus, such as, Freddie Mac computer should also own the underlying first mortgage, incase the foremost is paid off the next should be as well. It places Freddie Mac computer in almost the same credit exposure status as if it possessed a first home loan to the entire earliest-plus-next home loan number, i.elizabeth., as though a money-out refi was done.

This is certainly obvious in decision so you can limit the restriction mortgage-to-well worth (LTV) proportion to simply 80 per cent

Concurrently, Freddie Mac has long been conventional in borrowing from the bank risk urges to have a money-out refi, showing its dubious objective value, an interest reviewed less than. That it borrowing plan will also incorporate regarding pilot towards the mutual worth of the first and you will CES mortgage, which means that its 80 % maximum LTV is basically a whole lot more restrictive than what if not pertains to most GSE purchase mortgage originations, that will variety to 97 percent LTV on occasion.

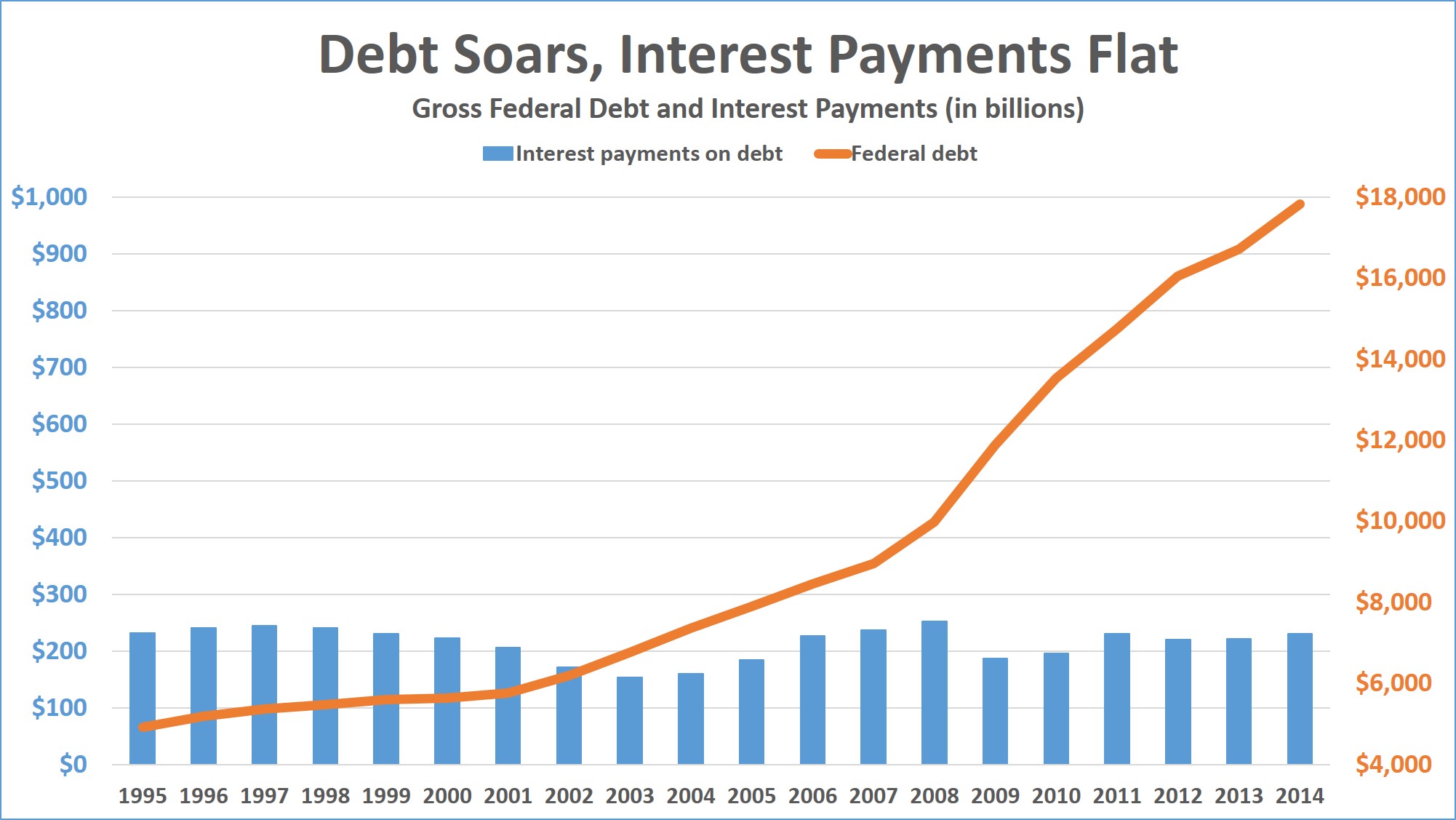

This means the brand new pilot is very credibly a secure and voice credit risk carrying out, suitable better in the enough time-mainly based risk appetite of your GSEs because they have conservatorship. a dozen

Mission: Security extraction things do not fit in this a good definition of the new GSEs’ homeownership purpose

The GSEs is actually hybrids created by Congress. On the one hand, they are built to end up being to possess-finances people had and you may capitalized from the private market investors trying to an excellent typical business go back. At the same time, he’s necessary to deal with a public plan mission one really does not create instance a return, leading to Congress as well as awarding them subsidies in order to preferably also they all-out. thirteen Regrettably, Congress failed to clearly explain the brand new GSEs’ mission from the laws and regulations starting Freddie Mac otherwise Federal check cashing near by me national mortgage association, leaving they as an alternative becoming discussed ultimately because of the their legislatively permitted affairs and a lot more general code. Because of this, determining the goal is somewhat subjective. 14

We do know, not, that FHFA has just reviewed and then categorized different items provided by new GSEs based on their quantity of mission intensity, which have verify commission cost becoming put lower on the extremely goal-intense and better with the minimum. The latter, possibly titled mission-remote points, include mortgage loans to your next land (we.e., not the main household regarding a manager-occupier), trader possessions mortgages, particular higher harmony mortgage loans and, away from brand of strengths to that particular blog post, cash-away refis. Leaving away highest balance mortgages, and this arise away from a necessity put of the Congress, it is probably a surprise to many subscribers the GSEs also offer 2nd family otherwise buyer assets mortgages. Simply because the fresh GSEs’ mission together with subsidies granted to are usually are not thought as aligned here at proprietor-occupied, primary home construction. As a result, new FHFA keeps cost large verify charges throughout these two situations. But at least these two items are completely regarding casing.